Last Updated: June 2026 | Author: Zee

For over 3.5 million Muslims residing in the United States, the holy month of Ramadan is not just a time of intense fasting, spiritual reflection, and community prayer; it is the most critical period of the year for charitable giving. Islamic tradition dictates that good deeds performed during Ramadan are multiplied seventy-fold or more, prompting the vast majority of American Muslims to discharge their annual religious financial obligations during this 30-day window.

However, navigating Islamic philanthropy within the framework of the United States financial and legal system requires strategy. Donors must balance strict theological requirements with complex modern assets—such as 401(k) retirement accounts, cryptocurrency, and real estate—while simultaneously maximizing their legal tax benefits. Before diving into the specifics of this holy month, we highly recommend understanding the foundational differences between secular and theological philanthropy in our overarching guide to faith-based and religious donations.

Whether you are preparing your philanthropic strategy for Ramadan 2027, calculating your annual Zakat, or looking for fully vetted 501(c)(3) Islamic charities, this master guide provides everything you need to purify your wealth, secure your spiritual rewards, and legally lower your US tax burden.

During the holy month of Ramadan, millions of Muslims in the USA fulfill their Zakat and Sadaqah obligations to maximize their spiritual rewards.

Phase 1: The Spiritual Multiplier of Ramadan

To understand why Muslim-American non-profits receive over 70% of their annual funding during a single month, one must understand the theological weight of Ramadan. In Islamic jurisprudence, a good deed is generally rewarded tenfold. However, during Ramadan, the Prophet Muhammad (PBUH) stated that performing an obligatory act (Fard) is equivalent to performing 70 obligatory acts outside of Ramadan, and performing a voluntary act (Sunnah) carries the reward of an obligatory act.

Furthermore, the last ten nights of Ramadan contain Laylat al-Qadr (The Night of Decree). The Qur’an explicitly states that worship and charity performed on this single night are “better than a thousand months” (approximately 83 years) of continuous worship. Consequently, American Muslims highly structure their charitable giving to fall within this month, setting up automated daily donations to ensure they catch this unprecedented spiritual multiplier.

Phase 2: The 4 Categories of Ramadan Giving

A common mistake made by new donors or those outside the faith is assuming all “charity” in Islam is the same. In reality, Islamic giving is divided into highly specific, heavily regulated categories. To ensure your donations are valid, you must direct your funds to the correct category.

Pro-Tip: Navigating Modern Zakat

Calculating Zakat in the modern American economy can be highly confusing. Before we break down the categories, watch this excellent explanation from Islamic Relief USA on exactly how your Zakat is calculated and distributed:

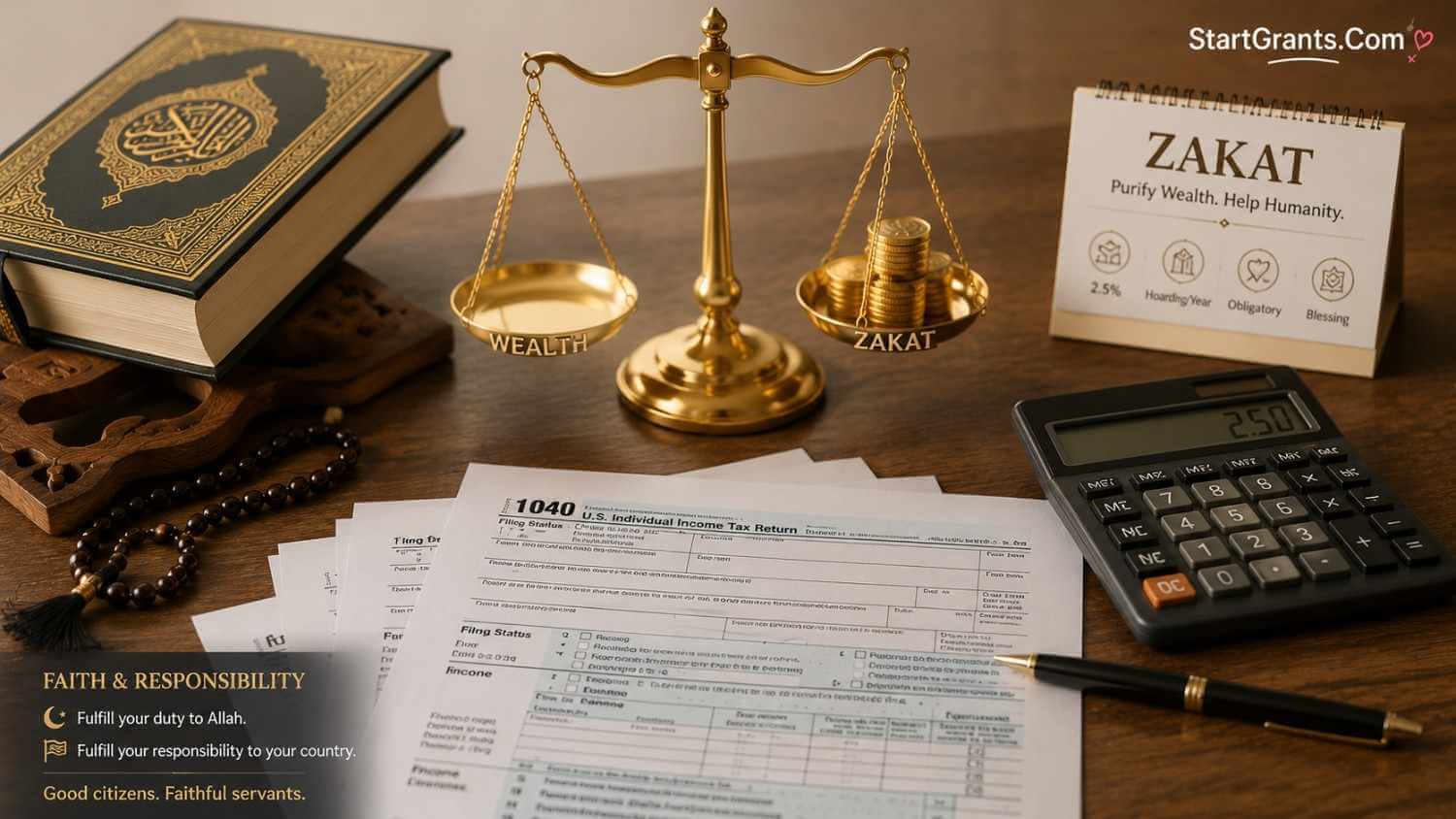

1. Zakat al-Mal (The Wealth Tax)

Zakat al-Mal is the third pillar of Islam and is an absolute, non-negotiable obligation for any Muslim whose stored wealth meets or exceeds the Nisab (the minimum threshold, traditionally equivalent to the value of 85 grams of gold or 595 grams of silver) for one full lunar year (Hawl). If you meet this threshold, you must pay exactly 2.5% of your qualifying surplus wealth.

In the United States, calculating Zakat al-Mal requires assessing various modern asset classes:

- Cash and Bank Accounts: All cash on hand, checking, and savings accounts are fully subject to the 2.5% Zakat.

- Stocks and Mutual Funds: If purchased for long-term investment/dividend yield, Zakat is only paid on the dividend income. If purchased for active day-trading (capital gains), the entire market value of the portfolio on your Zakat anniversary is subject to the 2.5% tax.

- 401(k) and IRA Retirement Accounts: This is a major point of confusion for American Muslims. Because you do not have immediate access to these funds without severe IRS penalties, many scholars rule that Zakat is only due on the withdrawable amount (the total balance minus early withdrawal penalties and minus estimated federal/state taxes).

- Cryptocurrency: Digital assets like Bitcoin or Ethereum are considered wealth. The total market value of your crypto wallet on your Zakat due date is subject to the 2.5% obligation.

- Business Inventory: The current market value of goods intended for sale is subject to Zakat. Real estate you live in or vehicles you drive are exempt from Zakat.

2. Zakat al-Fitr (Fitrana)

Unlike Zakat al-Mal, which is based on your accumulated wealth, Zakat al-Fitr (often called Fitrana) is a flat, per-person levy required from every single Muslim—regardless of age, gender, or wealth status—before the Eid al-Fitr prayer occurs at the end of Ramadan. The head of the household usually pays on behalf of their dependents.

The purpose of Fitrana is to ensure that the poorest members of the community have enough food to celebrate the Eid holiday, and to purify the fasting person from any idle or obscene speech committed during Ramadan. In the USA for 2027, major Islamic charities generally set the Fitrana amount between $12 and $15 per person, based on the local cost of a staple meal.

3. Fidyah and Kaffarah (Missed Fast Compensations)

Fasting during Ramadan is physically demanding. Islam provides merciful exemptions for those unable to fast, but these exemptions carry financial obligations.

- Fidyah: If a person cannot fast due to a chronic illness, old age, or pregnancy/nursing, and they cannot make up the days later, they must pay Fidyah. This requires feeding one poor person for every single day missed. In the US, this is typically calculated at $12 to $15 per missed day.

- Kaffarah: If a person intentionally breaks their fast without a valid religious excuse, the penalty is severe. They must fast for 60 consecutive days. If physically unable, they must feed 60 poor people, which generally equates to a penalty of $700 to $900 per intentionally broken fast.

4. Sadaqah & Sadaqah Jariyah (Voluntary Charity)

Any donation given above the mandatory Zakat limits is considered Sadaqah. During Ramadan, Muslims heavily invest in Sadaqah Jariyah (continuous charity). These are infrastructure projects that outlive the donor, providing continuous spiritual rewards (Hasanat) even from the grave. Popular Sadaqah Jariyah projects funded by US donors include building deep-water wells in drought-stricken African nations, constructing rural schools, or sponsoring the full medical education of an orphan.

Phase 3: Top Vetted US-Based Islamic Charities

The Qur’an strictly limits the distribution of Zakat to eight specific categories of people (the Asnaf), primarily the extreme poor, the destitute, and refugees. You cannot give Zakat to build a mosque, and a charity cannot legally use your Zakat to pay their CEO’s salary or fund their marketing budget.

Therefore, American Muslims must use charities that guarantee a “100% Zakat Policy” (meaning every penny goes directly to the end recipient) and possess a valid IRS 501(c)(3) status for tax purposes. Here are three of the most trusted organizations operating in the USA in 2027:

1. Islamic Relief USA (IRUSA)

One of the largest and most globally recognized Muslim humanitarian organizations, Islamic Relief USA boasts a highly coveted 4-star rating on Charity Navigator. IRUSA offers meticulously segregated donation portals, allowing you to specify exactly whether your money is Zakat al-Mal, Zakat al-Fitr, or general Sadaqah. Their domestic US programs heavily support local food pantries and disaster relief.

2. Zakat Foundation of America

Headquartered in Chicago, this organization guarantees a 100% Zakat distribution policy, taking absolutely zero administrative fees from Zakat donations. They are highly transparent and focus extensively on long-term sustainability projects, orphan sponsorships (Kafalah), and emergency refugee relief in conflict zones.

3. ICNA Relief

If you prefer your Zakat and Sadaqah to stay strictly within the United States, ICNA Relief is the premier domestic Muslim charity. They operate dozens of women’s transitional homes, free mobile medical clinics, and massive food banks in major US cities, serving the American public regardless of their race or religion.

Phase 4: Creative Ramadan Charity & Fundraising Ideas

If you want to go beyond simply writing a check, the holy month offers incredible opportunities for hands-on community engagement. Whether you are an individual looking for Ramadan charity ideas or a community leader searching for high-impact Ramadan fundraising ideas, activating your local network multiplies your spiritual reward.

1. Individual & Family Charity Ideas

If you want to involve your children and instill the value of Sadaqah:

- Iftar for the Unhoused: Partner with a local soup kitchen to sponsor or physically distribute hot Iftar meals to the homeless in your city.

- Eid Care Packages: Assemble gift baskets filled with toys, new clothes, and Halal treats, and deliver them to local refugee resettlement agencies to ensure newly arrived families can celebrate Eid al-Fitr with dignity.

2. High-Impact Fundraising Strategies

If you are part of a Mosque board or a Muslim Student Association (MSA) trying to raise capital during peak giving season:

- The 27th Night Crowdfunding Push: Leverage platforms like LaunchGood to run a peer-to-peer campaign. Capitalize on the spiritual urgency of the last 10 nights (seeking Laylat al-Qadr) by asking 100 community members to donate just $100 each on the 27th night.

- Corporate Matched Iftar Dinners: Host a formal community Iftar and secure a wealthy donor or local Muslim-owned business to agree to a “Donation Match.” Announce to the attendees that every dollar they pledge during the dinner will be matched 1-to-1 up to $10,000, instantly doubling your fundraising power.

Phase 5: US Tax Deductions for Zakat

Paying your Zakat to a registered 501(c)(3) Islamic charity in the USA not only purifies your wealth spiritually but also provides a legal tax deduction on your federal returns.

One of the greatest benefits of fulfilling your religious obligations in the United States is that the federal government actively incentivizes philanthropy. Your obligatory Zakat and voluntary Sadaqah are legally recognized as charitable contributions by the Internal Revenue Service (IRS), allowing you to significantly lower your taxable income.

1. The Requirement of 501(c)(3) Status

To claim a tax deduction, you absolutely must donate to a registered 501(c)(3) tax-exempt organization. If you send Zakat money directly to your impoverished relatives overseas via Western Union, or hand cash to a homeless individual on the street, it is not tax-deductible. While God accepts it, the IRS does not. Always ensure the Islamic charity or local mosque has a valid Employer Identification Number (EIN).

2. Standard vs. Itemized Deductions (Schedule A)

To claim your Zakat on your US tax return, you cannot take the “Standard Deduction.” You must choose to “Itemize” your deductions using IRS Form 1040, Schedule A. You should only itemize if your total deductible expenses (including your Zakat, state/local taxes, and mortgage interest) exceed the standard deduction threshold for that tax year. For wealthy Muslim Americans with high Zakat obligations, itemizing is almost always the financially superior choice.

3. Donating Appreciated Assets (The Halal Tax Loophole)

Many wealthy Muslims choose to pay their Zakat by donating appreciated stock shares or cryptocurrency directly to a 501(c)(3) Islamic charity. This is an incredibly powerful, entirely legal tax strategy. If you transfer stock that has gained massive value directly to the charity, you avoid paying capital gains tax entirely, and you get to deduct the full fair market value of the stock on your tax return. This effectively allows you to pay your Zakat using pre-tax dollars.

4. Donor-Advised Funds (DAFs) for Muslims

A growing trend among high-net-worth Muslim Americans in 2027 is the use of Shariah-compliant Donor-Advised Funds (like the American Muslim Community Foundation). A DAF allows you to deposit a massive lump sum of wealth (getting an immediate, massive tax deduction for that specific year), and then slowly disburse the money to various Islamic charities as Zakat or Sadaqah over the course of several years.

Phase 6: Avoiding Ramadan Charity Scams

Because the Muslim community is incredibly generous during Ramadan, scammers actively exploit this 30-day window. Fraudsters will create fake websites that mimic major Islamic charities or launch fraudulent GoFundMe campaigns claiming to support orphans in war-torn regions.

To protect your spiritual intention and your financial security, adhere to these strict vetting protocols:

- Verify IRS Registration: Before making a large Zakat payment, confirm the organization’s legal status directly through the IRS Tax Exempt Organization Search tool.

- Never Donate via Cash App or Zelle: Legitimate charities will never ask you to send Zakat to a personal phone number via peer-to-peer cash apps. Always donate through secure, encrypted portals on the organization’s official `.org` website.

- Verify the URL: Scammers often change one letter in a famous charity’s URL (e.g., changing `irusa.org` to `irusas.org`). Always double-check the address bar for the lock icon (HTTPS) before entering your credit card information.

- Demand a Tax Receipt: By IRS law, any charity accepting a donation of $250 or more must provide a formal, written acknowledgment. If an organization cannot or will not provide an official tax receipt containing their EIN, they are not a legitimate 501(c)(3), and your donation cannot be legally deducted.

Conclusion: The Ultimate Return on Investment

Ramadan is the ultimate spiritual and financial reset. By meticulously calculating your Zakat al-Mal, ensuring your family’s Zakat al-Fitr is paid before the Eid prayer, and investing in Sadaqah Jariyah, you are participating in a 1,400-year-old system of wealth purification and community care.

As an American Muslim, leveraging the US tax code by donating to registered 501(c)(3) organizations allows you to maximize your impact while legally reducing your federal tax liabilities. Use this 2027 guide to vet your charities, maintain meticulous records for the IRS, and ensure that your wealth serves as a bridge to Paradise rather than a burden on the Day of Judgment.

Frequently Asked Questions (FAQs)

Q1: Can I pay my Zakat in advance before Ramadan starts?

A: Yes. The majority of Islamic scholars agree that you can pay your Zakat in advance (even years in advance) if there is an urgent need in the community, such as a famine or natural disaster. However, when your actual Zakat anniversary date arrives, you must calculate your wealth to ensure the advance payment covered the full 2.5% obligation.

Q2: Is my Zakat tax-deductible if I send it to an overseas charity?

A: Generally, no. The IRS only allows tax deductions for donations made to US-based 501(c)(3) organizations. However, you can easily bypass this by donating to a US-based charity that operates internationally (like Islamic Relief USA or Penny Appeal USA). Your money still reaches the overseas crisis zones, but you receive the legal US tax deduction.

Q3: Do I have to pay Zakat on my 401(k) if I am not retired yet?

A: Yes, but the calculation is nuanced. Because a 401(k) is not immediately accessible without penalties, most modern Fiqh councils state you only owe Zakat on the “net cash-out value.” This means you calculate the total 401(k) balance, subtract the standard 10% IRS early withdrawal penalty, subtract your estimated income tax rate, and then pay 2.5% on the remaining accessible amount.

Q4: Can I give Zakat al-Fitr (Fitrana) to my local mosque’s construction fund?

A: Absolutely not. Zakat al-Fitr has one very specific purpose: to feed the poor so they do not go hungry on the day of Eid. It cannot be used to pay mosque utility bills, buy carpets, or fund construction. It must be given directly to the poor or to an agency that will purchase food for the poor on your behalf.

Q5: If I owe debts, do I deduct them before calculating my Zakat?

A: It depends on the type of debt. Short-term, immediate debts (like a credit card bill due this month or a utility bill) can be deducted from your total wealth before calculating Zakat. However, long-term debts like a 30-year home mortgage or massive student loans are NOT entirely deducted, as doing so would exempt people from Zakat for decades. You may only deduct the upcoming 12 months’ worth of mandatory payments.

Important Disclaimer: StartGrants.com is an independent information portal. We are not a religious fatwa council or a certified public accounting firm. Islamic financial rulings (Fiqh) differ among various Madhahib (schools of thought). Always consult your local Imam for personal Zakat calculations and a licensed CPA regarding IRS Schedule A tax deductions.

{kind=link}