Last Updated: July 2026 | Author: Munir Ardi

When financial disaster strikes—a sudden job loss, a medical emergency, or the threat of eviction—millions of Americans search the internet hoping to find a government grant to bail them out. The term “personal use grant” is highly sought after, but it is also one of the most misunderstood concepts in federal funding.

Let us be perfectly clear: the federal government does not issue checks directly into your bank account so you can pay off your credit card debt, go on vacation, or buy a personal vehicle. However, the government does provide billions of dollars in highly targeted financial assistance to help individuals survive critical hardships. These are officially known as subsidies, waivers, or direct assistance programs.

Before you begin filling out forms, you must understand the broader ecosystem of individual aid to ensure you do not fall victim to predatory scam websites. Calibrate your expectations by reading our foundational guide: Free Government Grants for Individuals: The 2026 Application Guide.

Applying for government grants for personal use requires matching your specific financial hardship with the correct federal or state assistance portal.

Phase 1: Decoding “Personal Use” Grants

If you search for how to apply for government grants for personal use, you must shift your vocabulary. Federal agencies distribute funds to states to handle local crises. Therefore, you are rarely applying for a “grant.” Instead, you are applying for a specific “benefit program.”

These benefit programs are designed exclusively for daily survival: keeping a roof over your head, keeping the heat on during winter, and ensuring your family has food. To understand exactly how these funds are distributed and to dispel the myth of random payouts, review our Tier-3 guide on how to get free money from the government legally.

Phase 2: Housing & Utility Assistance (Keeping Your Home)

The largest sector of personal assistance addresses the housing crisis. If you are facing eviction or cannot afford your utility bills, these federal programs act as massive personal subsidies.

1. Housing Choice Vouchers (Section 8)

Administered by the Department of Housing and Urban Development (HUD), this program assists very low-income families, the elderly, and the disabled to afford decent, safe, and sanitary housing in the private market.

How to Apply: You must apply through your local Public Housing Agency (PHA). Because demand is exceptionally high, waitlists can last for years, so it is critical to apply immediately.

2. LIHEAP (Low Income Home Energy Assistance Program)

If you cannot afford to heat your home in the winter or cool it in the summer, LIHEAP provides a direct grant. The money is not given to you; it is paid directly to your energy provider to prevent utility shut-offs.

How to Apply: LIHEAP is federally funded but state-administered. You must locate your state’s specific LIHEAP office (usually the Department of Health and Human Services) to submit an application during the open seasonal windows.

3. Weatherization Assistance Program (WAP)

This program reduces energy costs for low-income households by increasing the energy efficiency of their homes (e.g., installing new insulation, fixing HVAC systems). It is effectively a personal grant for home improvement that you do not have to repay.

Pro-Tip: Avoiding Scams During a Crisis

When you are desperate to keep the heat on or pay rent, you become a prime target for fraudsters. Scammers constantly evolve their tactics to steal your identity or charge fake processing fees. Protect yourself by watching this urgent update, New Scams to Watch Out For in 2025, before you submit your personal information anywhere online:

Phase 3: Healthcare, Disability, & Nutritional Support

Medical bills and the cost of groceries are the leading causes of personal financial ruin. The government provides several critical safety nets to offset these costs.

- SNAP (Supplemental Nutrition Assistance Program): Formerly known as food stamps, SNAP provides a monthly stipend on an EBT card. While it restricts purchases strictly to food items, it frees up your personal cash flow to pay for rent or debt.

- Medicaid & CHIP: Medicaid provides free or low-cost health coverage to millions of Americans. CHIP (Children’s Health Insurance Program) covers children in families that earn too much for Medicaid but too little for private insurance.

- HCBS Waivers: For disabled individuals or the elderly who require daily care, Home and Community-Based Services (HCBS) waivers act as personal medical grants that pay for in-home aides, preventing the need to move into an expensive nursing facility.

Phase 4: Educational Pursuits & Forgotten Assets

Sometimes, personal financial crises can be solved not through hardship grants, but by leveraging educational funding or recovering lost money.

If you are struggling to advance your career due to a lack of education, applying for the Federal Pell Grant or private institutional funding is your best path forward. Master the art of requesting educational funds by reading our guide on how to write bursary application letters.

Additionally, you may have your own “free money” sitting in government vaults. Forgotten utility deposits, uncashed paychecks, and abandoned bank accounts are held by state treasuries. Learn how to search the official databases to recover your money by reviewing how to check if you have assets in the US Treasury (unclaimed money).

Phase 5: The Official Application Process

The most dangerous mistake you can make when applying for personal grants is using a third-party, commercial website that charges a “processing fee.” Applying for federal and state assistance is always 100% free.

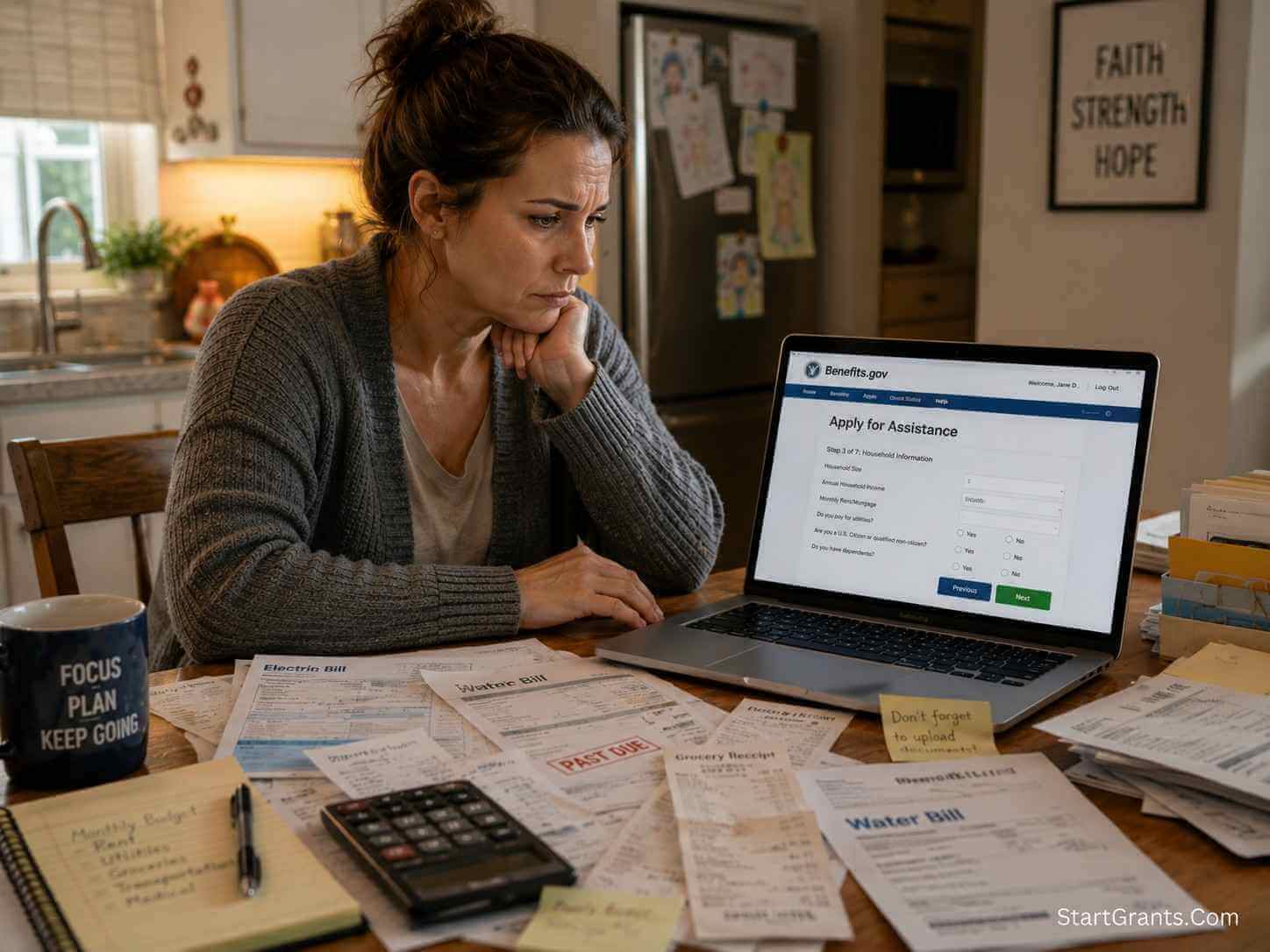

The U.S. government has centralized the discovery process. To find out exactly which of the programs listed above you qualify for, navigate directly to Benefits.gov. By using their free “Benefit Finder” tool and answering an anonymous questionnaire about your income, household size, and state of residence, the system will output a customized list of official links directing you to your local state agencies to begin your applications.

Pro-Tip: Navigating the Benefit Finder

The Benefits.gov platform is an incredible, free resource, but its extensive questionnaire can feel overwhelming for first-time users. To ensure you discover exactly which personal use grants you qualify for without missing any hidden programs, follow this official visual walkthrough, How to Use the Benefit Finder on Benefits.gov:

Phase 6: The Muslim Perspective (Halal Hardship Relief, Riba & Gharar)

For Muslims living in the United States, facing a personal financial crisis—such as an impending eviction or an unpaid heating bill—introduces a profound spiritual test. The Western financial system is designed to offer quick, debt-based solutions to personal emergencies, which requires extreme caution and steadfast adherence to Islamic principles.

The Trap of Riba in Personal Emergencies

When a family cannot afford their monthly utility bills, the most heavily advertised solution in the U.S. is the “payday loan,” a cash advance, or putting the debt on a high-interest credit card. In Islamic jurisprudence, utilizing any loan that mandates the payment of compounding interest is explicitly Riba. Engaging in Riba is considered one of the major sins (Haram) and removes the blessing (Barakah) from one’s wealth.

Therefore, applying for legitimate government grants for personal use—such as LIHEAP (for utility bills) or SNAP (for food)—is not merely an option; it is a Halal imperative. Because these government subsidies are classified as Hibah (gifts) and require no repayment with interest, they are a 100% permissible way to survive a crisis without compromising your faith.

Muslim families facing financial hardship must actively seek out Halal government subsidies or community Zakat to pay personal bills without falling into the trap of interest-bearing loans (Riba).

Zakat: The Ultimate Halal Safety Net

If you apply for government assistance and are denied, or if the waitlists (like Section 8) are too long, you must still resist the temptation of Riba-based debt. Muslims facing genuine hardship over basic necessities inherently qualify as recipients of Zakat (obligatory Islamic alms).

Instead of a commercial loan, individuals should immediately contact their local Masjid or national Islamic relief organizations. Entities such as ICNA Relief or the National Zakat Foundation (NZF) actively distribute Zakat funds to Muslim families in the U.S. specifically to cover emergency rent, food, and medical bills.

Navigating Mandatory Insurance (Gharar)

Many government housing programs, such as securing a subsidized apartment, mandate that the tenant carry renter’s insurance. Traditional commercial insurance is structurally problematic in Islam due to the presence of Gharar (excessive uncertainty) and elements of gambling. While true Islamic cooperative insurance (Takaful) for personal renters is still developing in the U.S., Islamic scholars widely permit taking the minimum required commercial insurance under the principle of Dharurah (necessity) to secure housing, urging Muslims to transition to Takaful options as soon as they become viable in their state.

Conclusion

Learning how to apply for government grants for personal use requires patience and a clear understanding of the bureaucratic system. You will not find a “random grant” to pay off consumer debt, but by utilizing Benefits.gov, you can access powerful federal subsidies for housing, healthcare, and daily sustenance to weather a financial storm.

For the Muslim community, navigating personal hardship must be done with spiritual integrity. By prioritizing Halal government assistance and community Zakat, and fiercely avoiding the destructive trap of Riba-based payday loans, you ensure that your path to financial recovery is both economically secure and divinely blessed.

Frequently Asked Questions (FAQs)

Q1: Can I get a government grant to pay off my credit cards?

A: No. The federal government does not issue grants to individuals to pay off unsecured consumer debt like credit cards, personal loans, or auto loans. Programs are strictly designed to assist with basic survival needs like food, housing, and medical care.

Q2: How much does it cost to apply for personal hardship grants?

A: It is absolutely free. You should never pay a processing fee, application fee, or “finder’s fee” to apply for federal or state assistance. Any website asking for your credit card information to secure a grant is a scam. All official applications are routed through `.gov` domains or local state agencies.

Q3: Can a single person with no children apply for SNAP or housing assistance?

A: Yes. While many programs prioritize families with children, the elderly, and the disabled, single adults without dependents can still qualify for programs like SNAP (food assistance) and certain housing vouchers, provided their income falls below the strict federal poverty guidelines for their state.

Q4: Is it Haram to accept SNAP (food stamps) or LIHEAP?

A: No, it is completely Halal. Accepting public welfare programs like SNAP or utility subsidies is permissible in Islam. These funds are distributed by the state for public welfare (classified as Hibah) and do not involve paying or receiving Riba (interest).

Q5: If I am facing eviction, should I take a payday loan or seek Zakat?

A: You should absolutely seek Zakat. A payday loan carries exorbitant, compounding interest, which is Riba and strictly forbidden (Haram) in Islam. If you are facing eviction, you qualify as needy (Al-Masakin). You should contact your local Islamic center or charities like ICNA Relief to request emergency Zakat funds to pay your rent ethically.

{kind=link}